Connecticut

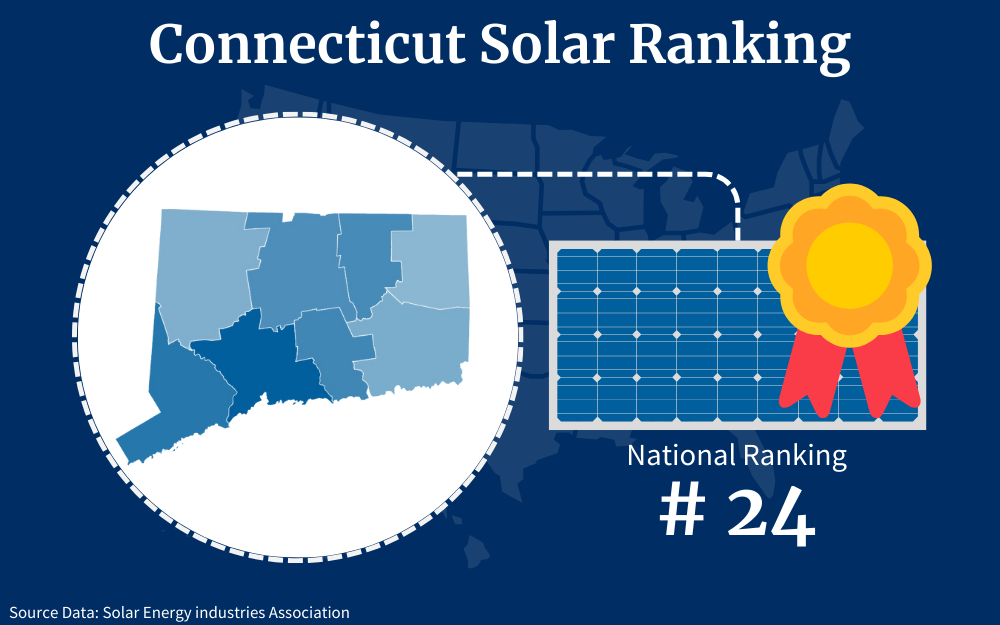

Connecticut continues to promote commercial solar deployment, though the overall solar capacity remains modest compared to national averages. As of 2024, Connecticut had more than 1,269 MW of distributed solar (systems generally up to 5 MW) installed across over 106,800 sites, producing an estimated 1.6 million MWh of clean electricity and displacing roughly 432,000 metric tons of CO₂, and ISO-NE projects total solar PV capacity could reach around 3,100 MW by 2034 under current trends. The state’s solar market overall ranked 27th nationally with roughly 1,902 MW installed as of mid-2025, according to SEIA data. To support commercial and municipal solar specifically, the Connecticut Green Bank doubled its financing authority for commercial-scale solar projects to $110 million, with $50 million dedicated to businesses, towns, and schools, already backing over 25 MW of commercial capacity via power purchase agreements.

State incentive programs continue to evolve but include specific deployment limits and carve-outs. Connecticut’s Community Shared Solar program (Shared Clean Energy Facility) was expanded to allow up to 50 MW per year of new clean generation (225 MW total over multiple years) with tariff support for subscribers, including small businesses, low-income households, and other customers. The Non-Residential Renewable Energy Solutions program has historically provided performance incentives for commercial projects (e.g., roughly 6 MW under certain funding levels as of recent PURA reports), with state-administered programs collectively having deployed hundreds of MW to date across residential, community, and non-residential categories. Additionally, state LREC/ZREC credits provide revenue to behind-the-meter commercial projects that generate renewable energy, helping offset costs.

Regulatory and fiscal trends reflect both support and new constraints. Connecticut has maintained property tax exemptions for commercial renewable energy sources, but is also adopting new tax frameworks—for example, a uniform solar capacity tax of $11,000/MW per year (with a 2 % annual increase) for systems over 2 MW approved after July 1, 2026—meaning larger ground-mounted commercial projects will face defined ongoing charges, with revenue directed to municipalities. At the same time, larger installations (typically > 1 MW) require review by the Connecticut Siting Council, not local zoning boards, which continues to shape deployment timelines and community engagement processes. Overall, Connecticut’s approach in 2026 balances continued financial support and clear deployment targets with new tax policy and siting oversight that influence how and where commercial solar projects are developed.

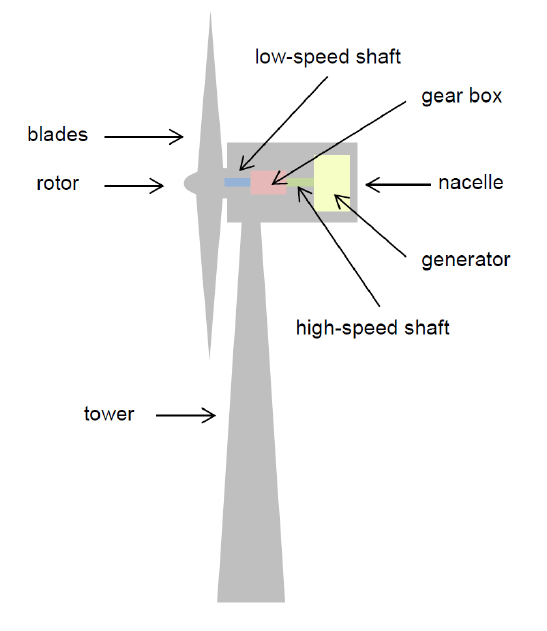

Commercial wind energy in Connecticut—especially large offshore projects—is a key part of its clean‑energy and climate strategy, but this stance has been tested by recent federal politics. The state has been actively planning and investing in offshore wind for years, including through its Offshore Wind Strategic Roadmap and the creation of the Connecticut Wind Collaborative to foster industry development, supply‑chain jobs, and regional economic benefits. Connecticut’s legislature and agencies have statutory authority to pursue several thousand megawatts of new offshore wind capacity to help meet its goal of a 100% greenhouse‑gas‑free electricity supply by 2040, and projects such as Revolution Wind were fully permitted and underway to deliver hundreds of megawatts of clean power to the New England grid.

Despite this proactive state policy, the pace and scale of commercial wind deployment in Connecticut have seen mixed results. In its latest competitive renewable energy procurement, Connecticut chose not to select any new offshore wind capacity, instead focusing on solar and energy storage, even as neighboring states secured thousands of megawatts of wind power. Officials framed the decision as part of a balanced approach to energy planning, but it temporarily slowed the expansion of new wind projects beyond Revolution Wind.

The state’s commitment has also been tested by federal interference and legal battles. In 2025 and early 2026, the Trump administration’s attempts to halt the Revolution Wind project—one of the first large‑scale commercial offshore wind farms serving Connecticut—triggered litigation in which Connecticut joined other states to challenge federal stop‑work orders. Federal courts have since blocked the halts and allowed construction to continue, a development Connecticut officials hailed as essential for energy affordability, grid reliability, and job creation. Public statements from the governor and attorney general underscored that Connecticut remains committed to advancing wind projects even amid political and regulatory uncertainty.

In 2026, Connecticut continues to take a proactive stance on commercial electric vehicle (EV) charging infrastructure, seeing it as a key part of its transportation and clean energy strategy. The Connecticut Department of Transportation’s revised National Electric Vehicle Infrastructure (NEVI) plan was approved by the Federal Highway Administration, unlocking roughly $52.5 million in federal funding to support the expansion of high‑speed DC fast chargers along major highway corridors. These funds are distributed as grants to private, public, and nonprofit developers — who build, own, maintain, and operate the chargers — rather than being owned by the state itself. This approach signals the state’s interest in facilitating commercial participation in building out a reliable, statewide charging network.

At the same time, Connecticut’s utilities, guided by the Public Utilities Regulatory Authority (PURA), continue to offer financial incentives for commercial EV charging projects under the statewide EV Charging Program. Administered by Eversource Energy and The United Illuminating Company, this program provides rebates that can cover a significant portion of costs for Level 2 and DC fast charging equipment and make‑ready infrastructure, with higher rebate caps for stations in underserved communities and incentives targeted to workplaces, fleets, public sites, and multifamily properties. However, recent state legislation taking effect in 2026 includes funding limitations and changes to rebate eligibility, prompting developers and businesses to submit applications before year‑end to take advantage of more generous incentive levels.

Despite this overall momentum, Connecticut faces some challenges in the commercial EV charging space. Policy changes have tightened the scope of certain incentive programs, and the timing of federal NEVI funding — influenced by broader national policy debates — adds uncertainty to longer‑term deployment beyond highway corridors. Nevertheless, state officials continue to coordinate with private partners and utilities to ensure that commercial charging infrastructure expands in a way that supports growing EV adoption while balancing fiscal and regulatory constraints.